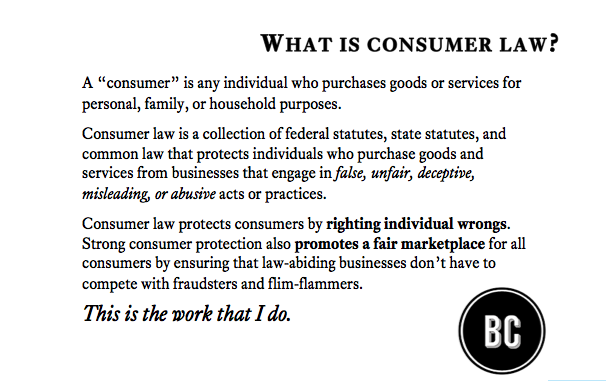

When people ask me what I do, I usually tell them, "I make bad jokes on the internet." When they ask me what I do for money, I tell them I'm a consumer lawyer. If they're not too proud to admit to not knowing what consumer law is, they'll ask, "What is consumer law?"

Here is a little mailer I sent out to fellow lawyers last year explaining what kinds of cases I handle as a "consumer lawyer".

Somehow, though, I think that just describing the kind of work that consumer lawyers do and the kinds of cases they take misses the point a bit. It gets to the what, but not the why of consumer law.

But, I recently had the opportunity to speak to about a hundred newly-minted attorneys at the KBA's New Lawyer Program about Kentucky consumer law. My Lebowski-themed presentation about consumer law touched on many of the same areas I listed in the mailer: the Kentucky Consumer Protection Act, debt collection abuse, insurance bad faith, auto fraud, the Kentucky Lemon Law, etc.

Before I ran through those specific state and federal statutes protecting consumers, though, I gave Kentucky's newest lawyers my freshest take on what consumer law is. I told them that being a consumer lawyer means applying all of your skill, training, and heart to the legal problems that impact low- and middle-income Americans. It means using the laws (common, local, state, and federal) to protect the bottom lines of the most fragile budgets in America.

Rather than defining consumer law as a kind of case or a particular set of statutes, I want to broaden my definition of consumer law to "practicing law with the goal of helping low- and middle-income American families achieve and sustain financial stability".

This definition allows me a broader self-concept of "what I do", aligns me more explicitly with the work of allies seeking those same ends through lobbying and public education efforts (rather than my more litigious efforts), and provides me a "North Star" when charting the work I want my firm to do. way forward for my firm. helps me evaluate the direction I want to take my firm. Anything that threatens the financial stability of economically vulnerable people—foreclosure, eviction, abusive debt collection, auto fraud, unfair or misleading business practices, repossession, bad faith claims adjusting from insurance companies—that's what I fight.

Practicing with a goal of helping people avoid the threats to their bottom line motivates me to pay attention to the evolving landscape of threats out there. Every year, it seems, there's a new problem, whether it's vacant and abandoned property, unpaid tax bills on real estate, starter interrupt devices on cars. There's a scammer born every minute.

Practicing consumer law is much, much broader than using the statutes we typically think of when we think of "consumer law" statutes. It means aligning yourself with economically fragile families and individuals and using the best, bravest version of yourself to defend them from the flinty-eyed predators stalking your clients and senseless corporate machinery that will consume them without ever thinking once.